What Constitutes A Successful Business Strategy?

A successful business strategy is a collection of purposeful decisions made by a company to maximize its value over a set period of time.

To maximize an organization’s value, a leader must manage their plans to get the most out of the strategic resources at their disposal. A strategic resource is anything that can be leveraged to increase an organization’s value: people, assets, knowledge, relationships, intellectual property, and so on.

For your business strategy to succeed, you must have a clear grasp of your objectives. Based on our comprehensive research into the topic, this article gives you an updated perspective on what a business strategy means for you as a business leader in today’s hyper-competitive marketplaces and how to develop one for your company.

Modern ‘Business Strategy’: Ten Universal Principles

In recent years, our knowledge of strategy has been significantly enhanced by the opportunity to observe the rise and fall of some of the best and most innovative companies over a longer period of time. In our view, a CEO must do only two things to be successful:

- Protect earnings from operating expenses and

- Maximize earnings growth over the foreseeable future

The defense-and-growth strategy is what increases an organization’s value over time.

In order to make money, there are only three key components: Price, Demand, and Cost, and accordingly, a good strategy is one that either sustains premium prices and superior levels of demand, or helps reduce unit costs.

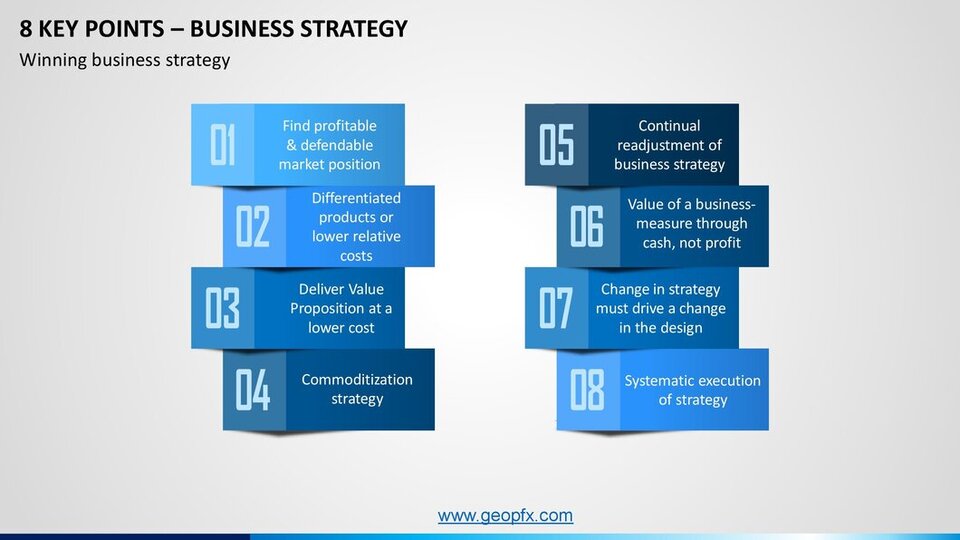

A business action that does not assist you in achieving any of these two objectives should not be considered part of your overall strategy. The following are eight key rules that must guide any business’s strategy:

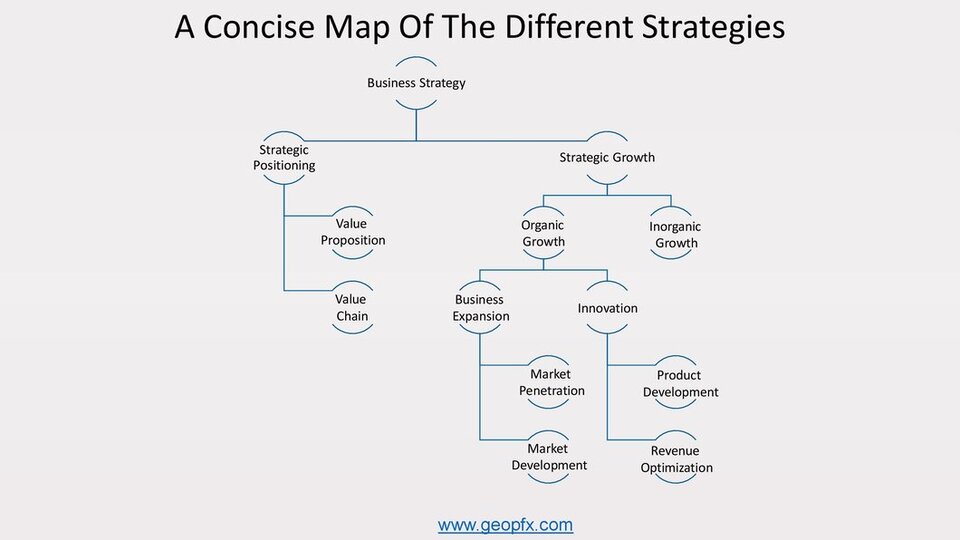

The only two ways to develop organically are through business expansions and innovations.

Questions to ask yourself about business strategy

- Are we doing all possible to maximize the wealth of our company in the foreseeable future?

- Are we on the “correct” path?

- Is our company in a good position in the market?

- Are we pursuing the “strategic” growth prospects that are suited for us?

- Is there any other way to progress?

The question of whether you end up outperforming or underperforming competitors, or whether your earnings come from markets close to or far from your core, becomes unimportant to your strategy as long as you’re trying to achieve the best return from your resources.

According to a recent Barclays survey, 47 percent of small business owners do not have a formal strategy in place to assist their company’s growth. Of the total, 25% have an informal, verbal business strategy, while the remaining 23% have no plan at all.

Barclay Survey

Types of Business Strategies

If a company’s products and services are neither unique nor valuable to the target market, or are in some manner difficult to imitate, the company’s market position could be compromised. As a business CEO, you have no choice but to defend a profitable market position with a differentiated Value Proposition and a distinct Value Chain.

Finding a successful business strategy & market positioning that can sustain and safeguard your organization is the issue you’ll confront while trying to strategically position your company. Target, the department store chain, is aware of Walmart’s successful business strategy, just as any furniture vendor is aware of Ikea’s plan, and yet they have all managed to carve out a successful niche in their own sectors that is tough to challenge or mimic.

As a result, strategic positioning for a firm is an iterative process that evaluates your company’s success and modifies course based on market changes.

Differentiation Strategy

The most profitable strategies are based on differentiation: providing clients with something they want that their competitors don’t. However, most businesses concentrate their efforts solely on their products or services in order to differentiate themselves.

A two-part framework can assist firms in identifying new areas of uniqueness and developing the ability to design successful differentiation strategies.

Consumption Chain Mapping

Trace your customer’s complete interaction with your product or service. Each product or service will have its own consumption chain. However, most chains share a few activities. If a business can make consumers aware of a need in a unique and thoughtful way, it can provide a tremendous source of uniqueness.

How do consumers realize they require your product or service?

Oral-B, a toothbrush manufacturer, figured out a method to profit from a consumer chain mapping practice. The company discovered a successful business strategy to have the brush itself speak with the client by using a trademarked blue dye in the center bristles of their toothbrushes. The dye gradually fades as the brush is handled. When the dye runs out, the brush is no longer usable and needs to be replaced.

How do customers find out about your product?

Making your product available when others aren’t (24-hour telephone order lines), selling your product in places where competitors don’t (small McDonald’s outlets in Wal-Mart shops), and making your product ubiquitous are all ways to differentiate on the basis of the search process (Pepsi).

How do customers arrive at their final decisions?

Customers at CarMax and AutoNation “sell” cars by allowing them to sit in front of a computer and define the characteristics they want in a car. They can then browse full descriptions of cars that potentially match their needs in private. Each vehicle’s final price is stated. After that, a sales assistant allows customers to check the vehicles that they are interested in and handles all of the paperwork if they decide to purchase one. The “selling” is done through the customers’ own choosing process, rather than by the salesmen.

What is the process for people to order and pay for your product or service?

Hallmark changed the way people order and refill products including greeting cards, gift wrap, giftware, stationery, electronic greetings, and decorations. Each store with which the company did business was equipped with computer terminals. The terminals connected those consumers to the company’s system directly, allowing for direct drop shipping and automatic restocking when inventories fell below a specific threshold.

What method do you use to deliver your goods or services?

Delivery allows for a lot of differentiation, especially if the goods is an impulsive buy or if the consumer need it right away. Because the warehouse and distribution centers are close to an Airborne Express hub, the incredible turnaround times are achievable. In a few of hours, packages can be picked up at the warehouse, transported to Airborne, and delivered to the consumer.

Post-delivery product or services

Every day, Progressive Insurance has a fleet of claims adjusters on the road, ready to respond to any automobile accident in their jurisdiction. They can keep track of everything they need and, in many cases, pay claims for policyholders on the moment. By removing the inconvenient and time-consuming aspects of traditional reporting, inspection, and assessment processes, the approach has considerably improved customer satisfaction.

What installation method do you use for your products?

Compaq provides consumers with a banner that clearly depicts the steps of installation. To make installation even easier, the company employs color-coded connections, cables, and outlets. It also has its computers set up such that when new users power on the system, a pleasant visual and audio presentation guides them through the setup and registration procedure.

What method of payment do you use to pay for your product or service?

Companies may discover ways to differentiate themselves by making the entire payment process easy to grasp for customers. With their payment practices, many businesses unknowingly generate enormous problems for their clients

What kind of storage do you have for your product?

Air Products and Chemicals, a manufacturer of industrial gases, built small industrial-gas plants next to customers’ site. Customers were satisfied, yet it resulted in higher switching costs.

Return and exchanges

When a product doesn’t work out, how you handle the situation might be just as important as addressing the need that prompted the purchase in the first place.

What methods do you use to repair or service your product?

Otis Elevator employs its remote-diagnostics capabilities to anticipate any service disruptions. Employees are dispatched to perform preventative maintenance in the evenings when traffic is light.

What happens when your product is no longer in use or gets disposed of?

Canon has devised a mechanism that allows users to send back used printer cartridges at no cost to them. After that, the cartridges are rehabilitated and resold. Customers can easily return used cartridges using this method.

Analyzing customer’s experience

Customers are constantly interacting with other people, places, events, and activities. At each point in the chain, such encounters determine the customer’s attitude toward your product or service. They can affect the dynamics of competition for that customer’s company when evaluated strategically.

This stage entails thinking about how a set of simple questions—what, where, who, when, and how—apply at each point in the consumption chain.

What?

- What do customers do at each stage of the purchasing process?

- What else do you think they’d like to do?

- What issues might they be having?

- Is there anything you can do to make their experience better while they’re at this point in the process?

Where?

- At this point in the consumption chain, where are your customers?

- Where else could they possibly be?

- Where do they want to be?

- Is it possible to get them to be there?

- Do they have any issues about their location?

Who?

- At any point along the chain, who else is with the customer?

- Do the others have any influence with the customer?

- Are their thoughts or concerns important?

- Who else could be with the consumer if you could make it happen?

- How may those other people impact the customer’s decision to buy your product if you could arrange it?

When?

- When are your clients at each given link in the chain—what time of day or night, what day of the week, what time of year?

- Is there a problem with this timing?

- When would they be at this link if you could arrange it?

How?

- How are your customers’ needs being addressed?

- Do they have any issues about how your firm is achieving their requirements?

- What other options do you have for attending to their needs and concerns?

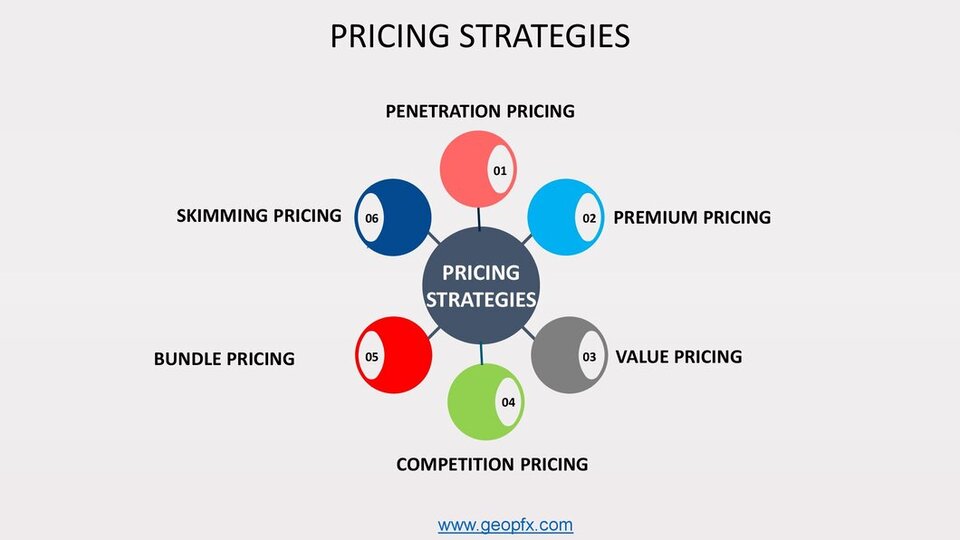

Price Leadership Strategy

The term “Price Leadership” refers to a situation in which the market’s dominant enterprise determines the price of goods or services. It usually occurs when the goods are homogeneous, that is, when the goods or services provided by different enterprises are same. As a result, customers have no preference and opt for the lowest price. In an oligopolistic market, where competition is low, such a model is common.

Price leadership is divided into three types based on the market parameters. They are as follows:

Barometric Model

In a barometer model, a company takes the lead in the industry by identifying and adjusting to changing market conditions. They create a reputation for being the first to notice and respond to these shifts. Even a small company can be a barometric price leader, and other large companies will follow them to match prices rather than waiting for such changes to happen. The pricing is quickly taken over by large corporations.

Example: Indigo Airline

Indigo Airline provided good service at a cost that was greater than that of smaller airlines but significantly lower than that of premium airlines. Other providers were compelled to change their prices and service quality to meet people’s needs in order to maintain market share.

Collusive Model

When companies with considerable market shares agree to fix the price of their goods at the same level, this is referred to as the collusive model of price leadership. To remain competitive in the market, smaller businesses must match the price leader’s prices.

The simplest approach to avoid this is for businesses to set prices in accordance to production costs and adjust accordingly. This strategy is commonly used in businesses where production costs are transparent and entrance costs are high, such as the aviation industry.

Dominant Model

According to the dominant model of price leadership, one company controls the majority of the market and is able to set the price, while all the other companies have to react to it. In this strategy, the large firm can purposely set the price low such that smaller competitors are unable to compete and may be forced to exit the market.

Reliance JIO started the network by giving its users free calls and internet. Other telecom behemoths were forced to reconsider and adjust their pricing in response to this move. JIO modified the cost of its products, which were no longer free but were moderately priced, after they had a large user base. Other networks were forced to modify their prices to match JIO’s rates in order to maintain their market share.

Strong firms frequently employ price leadership to demonstrate their market presence and dominance. Smaller businesses, on the whole, find it advantageous to follow a price leader in order to avoid losing money due to price wars. Advanced techniques can be used by ambitious firms to set the trend and predict inevitable industry developments.

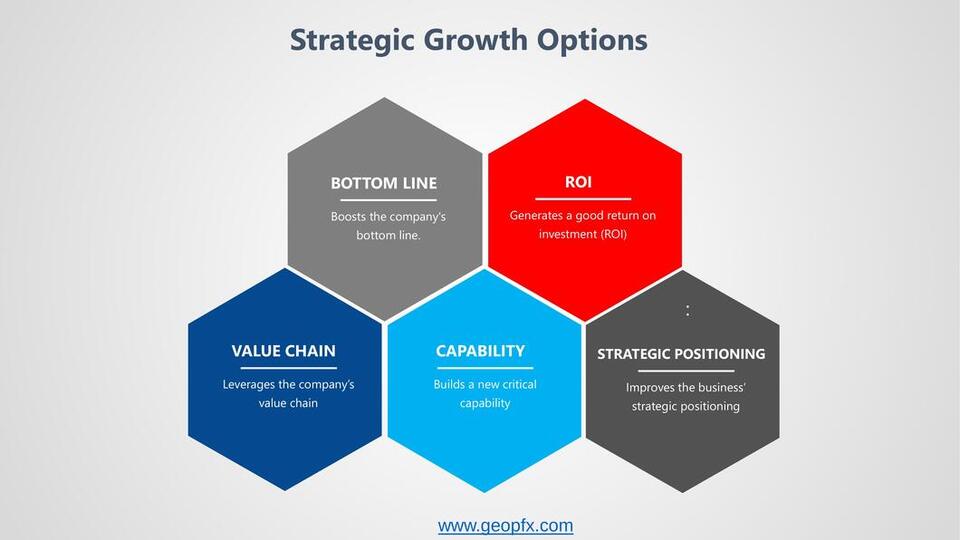

Business Growth Strategies

Growth isn’t always equal, and sales alone don’t always convey the whole story. To put it another way, increasing your top line (revenues) doesn’t always imply increasing your bottom line (profits). A $500 million investment yielding $10 million per year is not the same as a $50 million investment yielding $10 million per year.

If you are contemplating a growth opportunity for your business, you should consider whether the following conditions are met:

As a collection of business initiatives intended to increase the bottom line of an organization, a growth strategy could be thought of as a group of business initiatives aimed at increasing revenue or profits, however, we prefer to speak about a strategic plan to maximize the growth of an organization.

But what possibilities do you have for expanding your business and devising a successful business strategy?

During our study, we discovered seven different growth techniques for any business:

Conclusion

You may now use this strategy map to view a visual picture of the decisions you’ll have to make while creating a new successful business strategy.

We all know there’s a difference between doing it right and getting it done when it comes to strategy. Strategic management, capital allocation, and each of the seven paths to growth are essential to the success of your company. The execution of business strategic planning necessitates discipline, and senior executives are responsible for promoting practices that keep a team focused on the goal.

Do you want your business to be successful and outperform your competitors? GeopFX can assist in the development and implementation of a strong and successful business strategy that will result in above-average profits and returns.

[…] CEO's must do two things to be successful. 1.Protect earnings from operating expenses 2.Maximize earnings growth over the foreseeable future […]